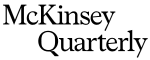

83 Q UA RT E R _ 0 2 _ 2 0 2 6 facilities; and a range of other advanced manufac turing, from pharmaceuticals to robots. EXHIBIT 1 Greenfield FDI is increasingly targeting future-shaping industries and the resources that power them. Greenfield foreign direct investment (FDI) announcements, by industry, annual average 2015–19 and 2022–May 2025, % of total 2015–19 2022–May 2025 Advanced manufacturing +142 Communications and software +73 Basic manufacturing –79 Operational and professional services –76 Metals and minerals +43 Energy +166 Conventional industries Future- shaping industries Resources Change, $ billion 1,137 Total, $ billion 1,407 1.1 % of GDP 1.3 25 20 11 17 4 23 14 14 10 24 7 31 - - - - - - - - - Note: For details, see Exhibit 2, “The FDI shake-up: How foreign direct investment today may shape industry and trade tomorrow,” McKinsey Global Institute, Sept 22, 2025. All $ figures are in terms of 2024 US dollars. Source: Using data provided by fDi Markets; McKinsey Global Institute analysis Cross-border investments in future-shap ing industries could substantially expand their capacity and shift their global footprint into new locations. Together, the industries that make up advanced manufacturing as well as communica tions and software (AI infrastructure) accounted for an annualized average of roughly $531 billion in announced greenfield FDI in the years since 2022. That is roughly 38 percent of announced FDI’s annual total of $1.4 trillion (Exhibit 1). In inflation-adjusted, 2024-dollar terms, this annual average climbed ten percentage points from 28 percent during the period from 2015 to 2019—the pre-COVID-19 period we use as a baseline for comparison. Of course, not every potential project sees the light of day, but past studies have found that FDI announcements reliably predicted capac ity creation on the ground, with realization rates between 60 and 80 percent. Tracking the announcement trends, AI data cen ters, semiconductor fabs, and EV manufacturing are all receiving much more investment. From 2022 to May 2025, roughly $115 billion per year was pledged to build new semiconductor fabs. Another $110 billion per year went to assembly lines for EVs and gigafactories for batteries—which are primarily used in automotive manufacturing but increas ingly relevant to broader applications in the realm of electrification. Amid the AI boom, data centers have received even larger pledges: equivalent to about $170 billion per year since 2022. This shift reflects the structure of these sec tors: They are winner-takes-most, technologically advanced, and capital intensive, so only a handful of global firms have the capabilities to compete. At the same time, governments, eager to host them and reduce reliance on geopolitically distant part ners, are deploying powerful carrots and sticks. The result is a surge of announced megadeals that drive most FDI growth and shape the global economy. In parallel, as energy- and material-hungry industries expand, resource sectors also are attracting growing investment. They include projects to extract and refine minerals critical to advanced manufacturing—for example, copper, lithium, and nickel—as well as new steelmak ing processes. Energy-related announcements also have risen. Here, announced investments in established renewable sources, like solar and

McKinsey Quarterly: A Time for Courage Page 84 Page 86

McKinsey Quarterly: A Time for Courage Page 84 Page 86